Background and rationale

SCAF1 mainly supports the development of utility-scale, grid-connected renewable energy projects in Africa and Asia. Specifically, SCAF supports private development companies (DevCos) already from an early stage of project development by co-financingsite identification, (pre-) feasibility studies, energy resource assessment, project design, environmental and social impact assessment, staffing and capacity building, etc. – activities for which other funding sources are extremely scarce (not to say non-existent), while DevCos themselves are typically small companies with limited equity/revenues and hence insufficient financial means to cover development costs fully on their own.

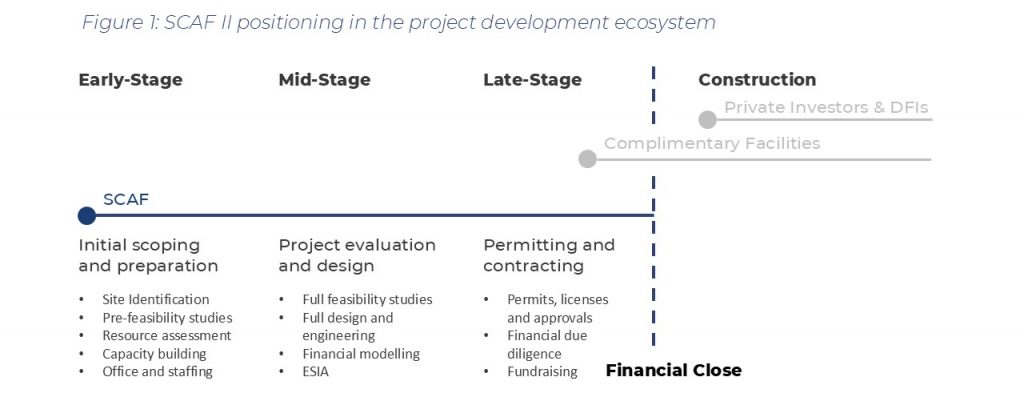

Figure 1 shows how SCAF support is instrumental for initiating project development. SCAF acts as market creator by financing the development of bankable projects for private investors and Development Finance Institutions (DFIs) that typically only enter at financial close (that is briefly before construction), as well as for other, later-stage-oriented (complimentary) investors to invest in development and construction at lower risk. No other facility or investor provides the required funding at such an early stage, enabling DevCos to develop projects in the first place and take the most promising ones through all phases to financial close.

SCAF offers separate support lines for pipeline and capacity building (SL1) and for developing specific projects (SL2), respectively. In its current form, SCAF provides grants, whereas SL2 funding needs to be paid back by the DevCos when a project reaches financial close.

Mobilising private capital and DFI funding at the project and corporate level

By filling the early-stage funding gap and supporting DevCos and projects moving towards financial close, SCAF has been a key enabler in de-risking projects and moving certain markets and DevCos up the maturity curve, as well as a key facilitator for mobilising private investments and DFI funding into DevCos and renewable energy projects in Africa and Asia.

Some key numbers and ratios speak for themselves: SCAF SL2 support of USD 2.8 million for nine specific projects enabled DevCos to develop 299 MW of renewable energy capacity to financial close, thereby mobilising USD 313 million from private investors and DFIs at project level (112x).

SCAF II support of USD 11 million has enabled DevCos to build strong project pipelines, internal capacities and hence trust in their abilities, which helped them raise another USD 1.1 billion from private investors and DFIs at corporate level (100x). The latter helps DevCos to operate on a more self-sustaining basis, that is to become more independent from donor support for developing project pipelines in future. While SCAF usually does not support corporate fundraising directly, its contribution to developing capacities, pipelines, and specific projects has been catalytic for DevCos to get these funds raised.

Priming new markets through lighthouse projects setting precedents

Several projects supported under SCAF were first-of-their-kind lighthouse projects that have had positive impact on the broader market by setting standards and demonstrating best practices for projects to come. For example, Kodeni Solar, a 38 MW PV plant developed by Africa REN in Burkina Faso, was the country’s first grid-scale PV project to reach financial close, and to date remains the country’s largest PV plant. The Dam Nai project, a 40MW wind farm in Vietnam developed by The Blue Circle was the country’s first internationally owned project and first project financed project in renewable energy in the country.

The potential and need for deploying renewable energy capacity in Africa and Asia is significant – yet untapped, mainly due to limited access to development funding

SCAF has been playing a significant role in developing projects, maturing DevCos and mobilising private-sector (and other public) capital for renewable energy deployment in Africa and Asia. It is important to understand though that energy sectors in many developing countries are – and are likely to remain – imperfect markets with deep-rooted challenges, high political and regulatory risks, significant fiscal constraints and poor macro-economic environments – all of which are macro issues that need to be tackled at another level. It would be presumptuous to believe that a facility like SCAF (given its limited mandate and budget) could initiate far-reaching political or economic change across the board.

The continuous need and justification for SCAF lies somewhere different. It is part of SCAF’s role to demonstrate that – despite all macro challenges and under challenging conditions that might persist – the development of large-scale renewable energy projects is possible. SCAF facilitates a way around existing challenges to “make things happen”. SCAF has helped to develop first-of-their-kind lighthouse projects with significant social and environmental impact and symbolic power. None of these projects would have been (or will in future be) possible without SCAF. There is no other facility that is willing to take on-board the same level of risks in these markets.

The above-mentioned challenges, the early-stage funding gap as well as the potential to develop demonstration projects and generate positive impact are not only expected to remain in several countries of the existing SCAF portfolio, but even more so in dozens of other markets that SCAF and its DevCo partners have not tapped into. To-date, SCAF supported 3.5 GW of development assets, which only represents a small fraction of the market. Since inception, SCAF has received requests for co-financing more than 16 GW of renewable energy projects.

The overall potential – and need – for developing and deploying renewable energy capacity in Africa and Asia is significant. According to the International Energy Agency (IEA), current annual investment in clean energy in emerging and developing economies (excluding China) is USD 260 billion and needs to reach USD 1.4-1.9 trillion by the early 2030s. The corresponding need for development capital can be roughly estimated at 5% or USD 70-95 billion.

Demand for support is increasing while public funds are increasingly scarce

Access to early-stage development capital remains one of, if not the key constraints for realising at least parts of this vast potential. SCAF partners and stakeholders (who are leading practitioners in their respective sectors and operating countries) confirm that currently only SCAF provides the missing piece of funding, that hardly any other source of capital is available for supporting early-stage project development, and that institutional investors rather provide construction capital (and perhaps some late-stage development capital) for projects that reach (or are close to) financial close:

- As opposed to the relative ease of raising construction financing, it remains very difficult to raise development capital for larger scale projects. This is evidenced by the actual installed capacity which falls a long way short of ASEAN renewables targets.” – Richard Aston, CFO at SCAF Partner Kairos Renewables

- “My impression is that there is very little access to at-risk capital for development functions. More specifically that the SCAF system is unique in its offering.” – Roanne Albertyn, Head of Investments Africa at SCAF Partner VS Hydro

- “There may be plenty of capital announced at a high level, but very little of it is actually deployable at the earliest stages, where it’s needed most. SCAF is among the very best facilities we know for addressing this gap — combining flexibility, responsiveness, and genuine risk sharing.” – Samuel Zekri, CEO at Hydroneo

- “I remain convinced that instruments like SCAF are highly relevant, especially in the current context.” – Gunter Fischer, Senior Investment Manager and Principal Advisor at European Investment Bank; longstanding member of SCAF Recommendation Committee

The continuous relevance of SCAF beyond 2026 is undisputed

Support needs for project development in Africa and Asia are expected to remain high, especially in times of increasing geopolitical uncertainties and protectionist policies. While there are several facilities, strategies and investors focused on financial close equity, only SCAF has a pureplay mandate on development. SCAF is necessary for the renewable energy ecosystem to continue to raise and deploy capital. Without SCAF, the MWs and capital deployed to-date would not have been achieved and tomorrow’s targets, especially in harder markets, will not be achieved. SCAF’s mandate talks to developing projects, but in practice, its impact as a market and ecosystem creator is far greater and more important.

[1] SCAF is a facility of the United Nations Environment Programme. Its second phase (2016-2026) was funded by the German International Climate Initiative (IKI) and the UK Foreign, Commonwealth and Development Office (FCDO).