By Fantine Dutronc and Indileni Nambala

The challenge: A systemic market failure

The deployment of renewable energy (RE) capacity in Africa and Asia is essential for providing access to clean energy and mitigating climate change. However – while institutional investors are ready to provide billions of dollars for the construction and operation of renewable energy projects – most developers of utility-scale, grid-connected projects face severe challenges in financing the development of bankable projects in the first place.

GHG mitigation is often not constrained by a lack of resource potential, policy ambition, viable project opportunities or investor interest, but by structural financial barriers that prevent projects from progressing through different development phases up to financial close. Financing for development activities (such as resource assessment, feasibility studies, ESIAs, grid studies, permitting, and fundraising) is scarce due to high perceived risk, long and uncertain timelines, and the absence of immediate revenue streams. Investors tend to “sit and wait” for the projects to come out of the development funnel rather than actively creating (investing in) their own pipeline. The result is a development-stage bottleneck creating a shortage of bankable projects, preventing billions of dollars from being invested into clean energy and the associated CO₂ emission reductions.

The primary constraints of many project developers are their cashflow shortages and limited balance sheets. These prevent them from developing projects from early stage down to financial close – let alone from developing multiple projects in parallel. Most of them are small or mid-sized enterprises with limited corporate equity, irregular revenue streams, high upfront cost exposure, that face long development cycles and restricted access to external working capital. Although development typically represents only ~5% of total project costs, it carries the highest risk and is therefore the most difficult phase to finance.

Addressing the early-stage funding gap

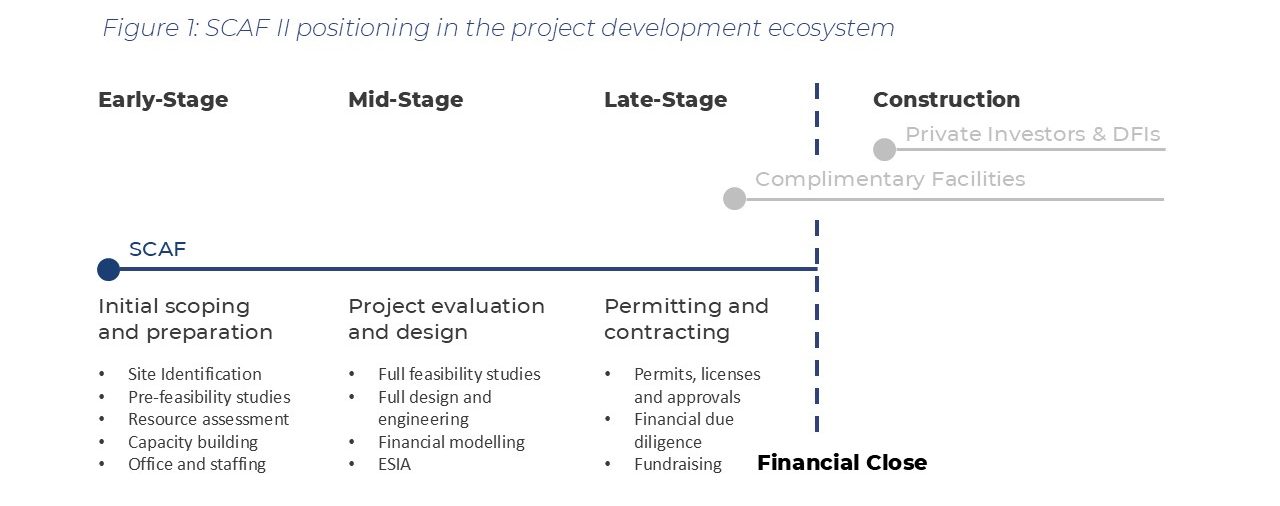

The Seed Capital Assistance Facility (SCAF)1 was specifically designed to address this systemic market failure that prevents renewable energy projects in emerging markets from reaching bankability. SCAF addresses the early‑stage funding gap that prevents technically and commercially viable projects from being developed towards financial close. Thus far, SCAF has used grants and repayable grants toco-finance critical development activities from early to late stage – such as feasibility studies, ESIAs, grid studies, permitting, legal structuring, and lender due diligence – while also providing corporate-level support that enabled developers to build teams, strengthen internal processes, and advance multiple projects in parallel.

SCAF’s catalytic role is well evidenced:

- Supported more than 3.5GW RE capacity via 55 mid-to-late-stage projects — 15 of which reached financial close by end of 2025; in addition, helped developers building internal capacities (teams, E&S standards, etc.) and early-stage pipelines of almost 100 projects.

- Less than USD 50 million in grants mobilised more than USD 2.6 billion from DFIs and private investors across supported funds, projects and corporate (developer) levels.

- Supported first‑of‑their‑kind lighthouse projects that reshaped and set standards in national markets (e.g., Dam Nai Wind Park in Vietnam, Kodeni Solar Plant in Burkina Faso, Golomoti Solar + BESS in Malawi).

- Capacity-building and local ecosystem development: SCAF-supported developers have grown into regionally recognised market makers in East Africa, Southern Africa, the Philippines, Vietnam, and Indonesia.

Besides being reassured that the lack of development financing is the most persistent barrier to renewable energy deployment in emerging markets, another lesson learned from SCAF’s second phase (2016-2026) was that grant-based instruments alone are insufficient and not suitable anymore to scale development support once developers and markets reach a certain level of maturity; moreover, high repayment rates of SCAF grants (at project financial close) have demonstrated borrower discipline and confirm the viability of debt instruments in development financing.

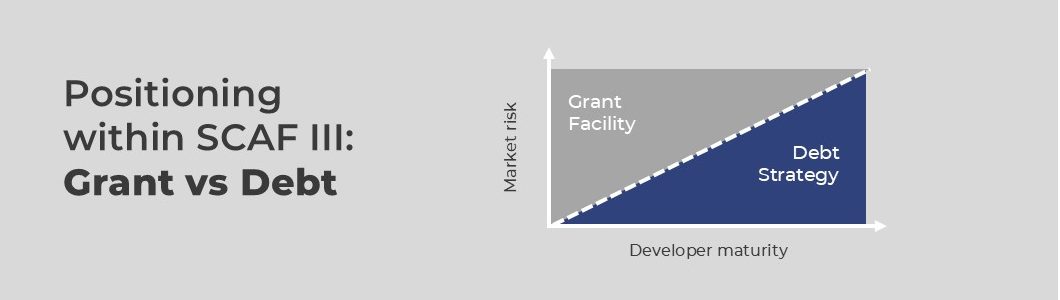

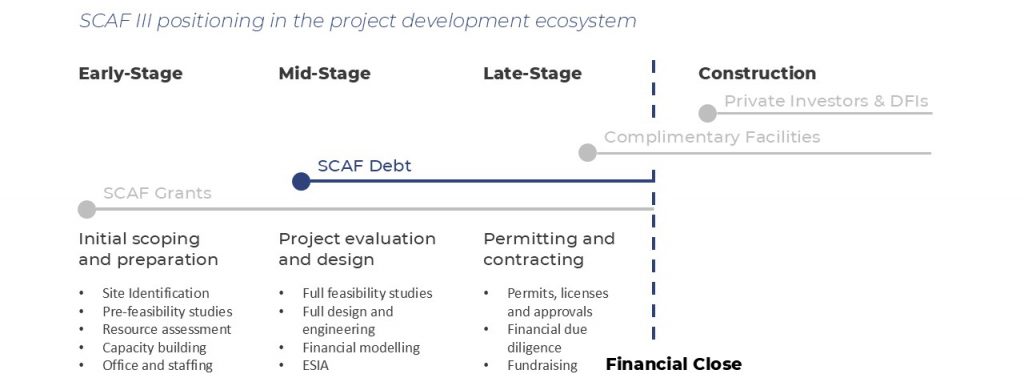

SCAF III – Grant and Debt

Entering into its third phase, SCAF III will be designed to continue addressing the same barriers, while adapting the instruments to evolving market conditions and developer needs. While grant-based support remains essential for smaller developers and frontier markets, SCAF III introduces a complementary Debt Strategy to address the persistent lack of risk-tolerant development-stage capital for more mature developers operating in lower-risk emerging markets. Through a blended finance structure, SCAF III will enable the offering of corporate-level development loans that directly address developer liquidity constraints, and the financing gap that prevents projects (i.e. an increased, scaled number of projects) from reaching bankability stage.

Even the more mature developers that operate as independent power producers (IPPs) or platforms – many of which have larger balance sheets and institutional backing – face constraints in making their own capital available for the actual development of new projects; return expectations and risk appetite of shareholders often require them to focus primarily on construction and operations. Having access to lower-cost development debt funding would enable these developers to scale their development activities, thereby accelerating the deployment of clean energy and associated GHG emissions mitigation.

Thus far, dedicated debt financing for project development remains largely unavailable, both internationally and locally. If any, institutional investors provide funding for the very final stages of development, once projects are largely de-risked and close to construction. Larger (local) commercial banks increasingly finance construction activities, but generally do not offer development-stage debt, and their working capital facilities are insufficient to support extensive development activities. The SCAF III Debt Strategy is specifically designed to address this barrier and to provide developers with the much-needed capital for mid-to-late-stage project development.

Developer profile

Key distinction compared to the existing (and continuing) SCAF Grant Facility is that developers supported/financed under the SCAF III Debt Strategy must be established companies with demonstrated execution capacity and later-stage pipelines in comparatively mature markets. They must have a proven track record of bringing projects to financial close and, in case of an IPP, through construction and into operation. These companies have typically evolved beyond early-stage, grant-dependent development but have not yet reached a scale where development activities can be fully self-financed – or where other debt sources are readily available. Developers in this group have a portfolio of operational assets, experienced multi-disciplinary teams often with project development, EPC and O&M functions, which provide a diversified revenue stream for the developer.

A defining feature of developers targeted by the SCAF III Debt Strategy – and a key difference to companies supported under the SCAF grant scheme – is the existence of a robust, later-stage development pipeline, rather than reliance on single-project success. To manage inherent development risk, these developers (need to) pursue multiple projects in parallel, accepting that not all projects will progress to construction (in planned time).

Relevance of the SCAF III Debt Strategy

Even for established developers, development-stage financing remains the principal bottleneck. Commercial lenders and infrastructure investors typically avoid financing pre-financial close risks, require construction-ready projects and do not provide corporate development loans. As a result, developers often face constraints on parallel project development, slower progression of projects to financial close, and pressure to dilute equity or sell projects prematurely.

The SCAF III Debt Strategy directly addresses these constraints by providing corporate-level and mid-to-late-stage development debt, enabling established developers to advance multiple projects concurrently, bridge the period between mid/late development and financial close, retain value and reduce reliance on early asset disposals, and, if required, strengthen internal development capacity and systems.

1 SCAF is a facility of the United Nations Environment Programme. Its second phase (2016-2026) was funded by the German International Climate Initiative (IKI) and the UK Foreign, Commonwealth and Development Office (FCDO).